06/30/2016

Donald Trump has proposed taxing remittances to pay for, among other things, a border wall. The Main Stream Media has reacted with hysteria. But it’s very doable, and I can tell you why.

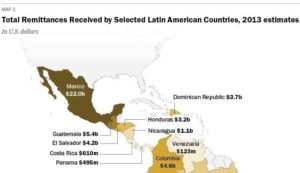

From 1997 to 2003 I, along with my ex-husband, owned a small mom-and-pop type store selling goods imported from Mexico. Most of our clientele was from Mexico with a small portion coming from Central America, Cuba, and even South America. One of the services we offered: wire transfers or sending money to said countries in Latin America. During the six years that we did this, we probably did somewhere between 42 to 45,000 transfers, sending on average $1.25 million a year out of the country.

Although we worked with Moneygram, most of the transfers we did were with smaller regional money transfer companies with names like Orlandi-Valuta, Tex-Mex, American Money Transfers, Global Transfers, and Cervantes.

Shortly before we quit the business, we were audited by the IRS for compliance with the Patriot Act. We were audited not because we’d done anything wrong but because we did more transfers than anyone else in our area. We passed the audit with flying colors.

Because of this experience, I think that I can authoritatively speak to the comments made by those in the Open Borders crowd that claim taxing remittances would be impossible. Mr. Obama seems to think this. Journalists like Jennifer Rubin writing on NJ.com [Trump’s (latest) nutty idea: Impound remittances to Mexico to pay for wall, April 5, 2016] and Victoria DeFrancesco Soto of NBC [Opinion: On Immigration, Remittances and Walls Miss the Point, April 13, 2016] want readers to believe taxing remittances is so difficult it’s not even worth trying.

Baloney. Of course remittances can be taxed. And it wouldn’t be difficult.

When a money transfer is sent, the remitter has to pay a fee for doing so. For example, a typical transfer amount would be $100. We would have charged $10 to send it out of the country. We would also have charged a tax on the amount charged for the service. In the county and state where I lived at the time, that would have been about a 5.5% tax on the $10 sending fee.

We would fill out a form with the remitter’s basic information like name, address, telephone number, etc. We would also have to ask for the receiver’s name, address, phone number, and the location (bank, telegraph office, etc.) in the city and country where they would like to have the receiver pick up the money.

On amounts less than $300, we were not required to ask for identification. However, because the money transfer business generally operates with lots of cash, and sometimes you cash checks for customers and there are lots of shady customers, we always asked for identification for any amount.

At $300, the federal government requires that you ask for a legal form of identification and put the number (passport, visa, driver’s license number) on the form. At amounts of $1000 or above, you are required to ask the occupation of the sender and to make a photocopy of the identification and fax it, along with a copy of the senders’ wire transfer form, to the IRS. [See MoneyGram’s Manual on compliance: PDF]

At the end of the day, you total up the amounts collected for transfers for each company. The next day, you deposit them to a special bank account that is set up just to collect the funds for each company. The amount deposited includes the original transfer amount, the fee charged for sending it and the tax on that fee. At the end of each month the transfer agent receives a commission check for the transfers done.

Usually we would earn about $2 — $3 of each transfer fee. The parent company is charged with paying the consumer tax on the fee. They are generally required to deposit the tax levied on the transfer fee once a month to a special account set up by the government for just that purpose. It’s just like when one has to pay FICA on an employee.

It would be easy to charge a 10 to 15% remittance tax on money transfers. All that would change is that the transfer agent would be adding another line to the intake form for the transfer, where he would calculate the amount of the transfer that would go toward a remittance tax. He would still do deposits in the same way. It would fall to the parent company to make the appropriate deposits to the IRS or federal agency charged with collecting the tax.

Remitters have to indicate the country to which the money is going all the time anyway, so identifying remittances to Mexico would be easy. Deciding who is here illegally is easy as well. All that would have to change is that, instead of requiring identification at $300, one would require it on all transfers. As I mentioned above, many transfer agents do this already.

If people are here legally, they will have a passport and a US government-issued visa. If they are here illegally they will have a matricula consular, something similar or no identification at all — or they’ll have a false one. And in my experience, the fakes aren’t difficult to spot.

Then all one would have to do is check a box indicating the form of identification along with its control number; or that the person does not present an identification. And if they don’t have an ID, well that’s probably because they’re here illegally.

In New Mexico, when you open a business, you are required to attend a workshop where tax specialists from the Taxation and Revenue Office teach you how to calculate and file state taxes. The first thing they say is that there is no sales tax in NM because that would be a tax levied on the consumer. Rather, there is the gross receipts tax and this is defined as follows: “a tax levied upon the business owner for the privilege of doing business in New Mexico.”

The remittance tax could have similar wording. For example, it could be defined as a tax levied upon the remitter for the privilege of earning money in the United States and the privilege of being able to send that money outside of the country for the benefit of foreign nationals — at the cost of advantages lost to the American citizen because money earned in his local community is not benefiting his community but is instead benefitting foreign nationals who have no stake or responsibilities in the US.

This is reasonable because frequently the money sent out of the country is taken directly from cash wages earned here and never circulates in the local economy, nor has taxes paid on it. It never benefits American citizens.

At the same time, the remitter is benefiting from living in the US because he or she is able to live in a country that is relatively safe and that has good infrastructure and that provides health and educational opportunities for the immigrant and his family members — many of whom are here illegally.

On top of that, the remitter frequently receives a healthy tax refund because he often claims not only dependents living here but dependents living in the home country. This is certainly the case with Mexicans living in the US.

So the remitter is winning both going and coming. And the American citizen is losing both coming and going. Because of this, I think that a 15% tax on all remittances sent outside of the United States is quite reasonable and not excessive at all, regardless of whether or not the remitter is here legally or not.

Sometimes the defenders of illegal immigration claim that if a remittance tax were imposed people living here illegally would just find another way to send the money. But this is another fake argument. The reason that the current remittance system is so well-developed is because back in the 1990s the unmet need existed for it.

Immigrants, legal and illegal, would try to send money back to the home country with relatives or friends. But often it never got there, because of foreign official corruption and extortion or just plain theft by foreign national thieves who preyed upon returning nationals who’d been visiting abroad.

Also, there are limits to how much cash you can physically take out of the country without reporting it. The more cash you carry on your person, the bigger a target you are.

Immigrants might try this method again — but they will quickly learn that the cost of trying to avoid the remittance tax will most likely be higher in terms of money lost or fees paid to those who try to take physically the money to the home country. The current money transfer infrastructure is fast (20 — 30 minutes), safe and extensive. People will realize that, despite there being a remittance tax, in the long run it will be cheaper and safer and it’s guaranteed to get where they want it to be.

I personally think that the fees charged ($4.99 — $9.99 per $100 to $300 sent) are too low for the work that is involved in doing the transfer, so a remittance tax of 10 to 15% per $100 wouldn’t be felt much. At first, people will whine, but they’ll get used it.

And it would be helpful to point out publicly that being able to live in the US and earn money and send it out of the country is a privilege. Sometimes, I would actually point this out to our customers — and, surprisingly, some agreed with me.

When Barack Obama and his Open-Borders shills in the MSM talk about the difficulty or impossibility of taxing remittances I wonder if they are embarrassingly ignorant, pitiably stupid, or willfully deceitful. We’re living in the 21st century. Haven’t they heard of databases, spreadsheets and adding machines? Don’t they know what the job responsibilities and skills of bookkeepers and accountants are? Databases can keep track of who sends what where and in what amounts. They can easily keep track of wire transfer amounts and the amounts levied upon them.

When I had my business, I regularly used a database to keep track of where we sent transfers because I wanted to know who my customers were and where they sent money. I used spreadsheets to calculate how much we had sent every month and what commissions we could expect.

Bookkeepers are trained to journalize all this information. Accountants are trained to figure out how to implement tax requirements.

Don’t listen to what the Ameriphobes would have you believe. Taxing remittances is not difficult. It wouldn’t be a problem. It would be a solution.

M. A. Gonzales [Email her] is a Mexican-AMERICAN who is voting for Donald Trump.